What is the Industrial Absorbents Market Overview – definition, scope, and significance?

The Industrial Absorbents Market comprises products designed to capture liquids, oils, and hazardous chemicals in industrial settings. It includes universal, oil‑only, and hazmat/chemical absorbents offered as pads, rolls, pillows, booms, and socks. The market serves oil & gas, chemical, food processing, healthcare, and automotive sectors, helping companies meet safety regulations, protect equipment, and reduce environmental impact. Its significance lies in safeguarding personnel, minimizing downtime, and supporting compliance with increasingly stringent spill‑control standards.

What are the key drivers, restraints, challenges, and opportunities shaping the Industrial Absorbents Market?

Drivers include rising industrial activity, stricter environmental legislation, and heightened awareness of workplace safety. Restraints stem from high material costs and competition from reusable containment solutions. Challenges involve supply‑chain volatility and the need for rapid product innovation to address emerging contaminants. Opportunities arise from the growth of oil‑rich regions, demand for eco‑friendly absorbents, and digital integration of spill‑management systems that can boost market adoption.

What current and emerging growth trends are influencing the Industrial Absorbents Market?

Current trends feature a shift toward high‑absorption capacity materials such as advanced meltblown fibers and bio‑based polymers. Emerging trends include smart absorbents with embedded sensors for real‑time spill detection and the adoption of modular spill kits that combine multiple product types. Manufacturers are also expanding into customized solutions for niche applications like pharmaceutical manufacturing, reflecting a move toward greater product specialization.

How has COVID‑19 impacted the Industrial Absorbents Market and what is the recovery trajectory?

The pandemic caused temporary disruptions in production and logistics, leading to short‑term inventory shortages. However, the heightened focus on hygiene and contamination control in healthcare and food processing accelerated demand for reliable absorbents. As supply chains stabilize, the market is experiencing a strong rebound, supported by renewed capital spending in oil & gas and chemical sectors, positioning it for sustained growth.

Who are the major competitors and what does the competitive landscape look like in the Industrial Absorbents Market?

The market is moderately consolidated, led by multinational companies such as 3M Co, Ansell Ltd, and Brady Corp, alongside specialized firms like SpillTech Environmental Inc and Oil‑Dri Corp of America. Competitive strategies include product innovation, geographic expansion, and strategic partnerships. Recent mergers and acquisitions signal a trend toward consolidation, allowing firms to broaden their product portfolios and strengthen distribution networks.

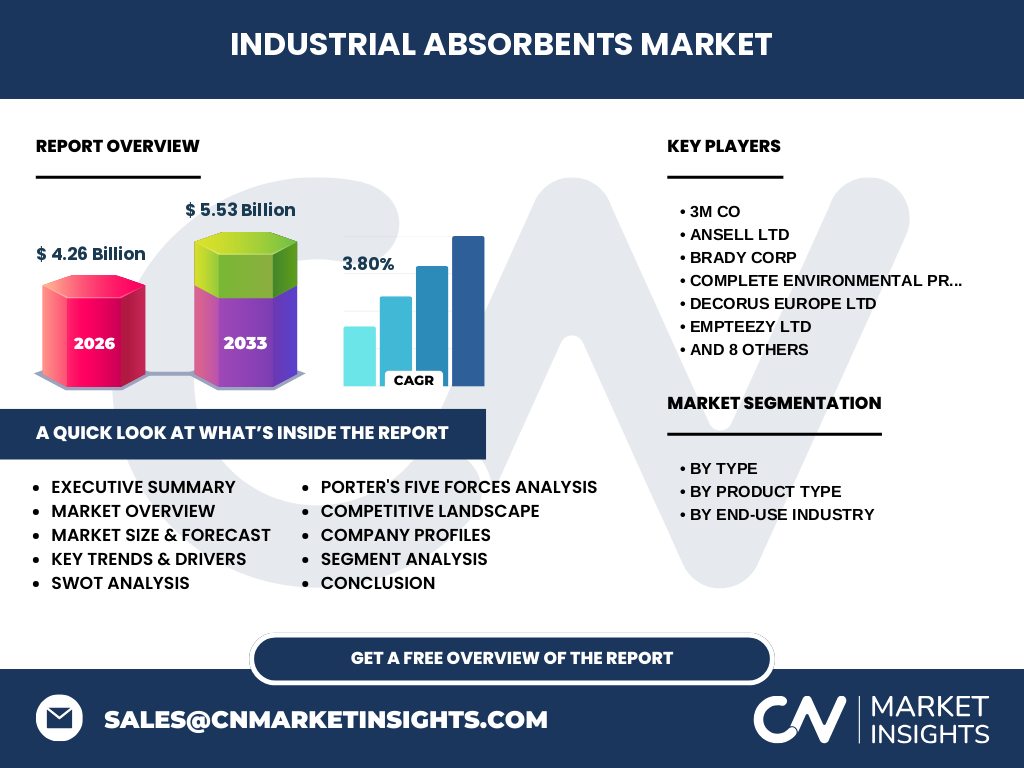

What are the high‑level findings and key takeaways presented in the Executive Summary?

The Industrial Absorbents Market is valued at $4.26 billion in 2026 and is projected to reach $5.53 billion by 2033, reflecting a CAGR of 3.80 %. Growth is driven by regulatory pressure, expanding end‑use industries, and technological advances in absorbent materials. The market shows a balanced mix of global leaders and niche players, with strong regional demand in North America, Europe, and emerging Asian economies.

What are the forecast projections for the Industrial Absorbents Market from 2025 to 2032?

Based on the provided data, the market is expected to grow from a 2026 base of $4.26 billion to $5.53 billion by 2033, indicating consistent expansion throughout the 2025‑2032 horizon. The 3.80 % CAGR suggests steady demand across all product and end‑use segments, with particular acceleration anticipated in oil‑only and hazmat absorbents as industrial safety standards become more rigorous.

How is the Industrial Absorbents Market sized and shared by type, product, and end‑use segmentation?

Segmentation spans three primary dimensions. By type, the market is divided into universal, oil‑only, and hazmat/chemical absorbents, each catering to distinct spill scenarios. By product, offerings include pads, rolls, pillows, booms, and socks, providing flexible deployment options. By end‑use, the market serves oil & gas, chemical, food processing, healthcare, and automotive sectors, reflecting broad applicability across high‑risk industrial environments.

What is the global geographic distribution of the Industrial Absorbents Market size and share?

The market exhibits strong presence across North America, Europe, and Asia‑Pacific, with notable demand in oil‑rich regions and industrial hubs. While precise regional values are not disclosed, the overall growth trajectory indicates balanced contributions from mature markets such as the United States and Germany, alongside rapid expansion in emerging economies driven by infrastructure development and increasing regulatory compliance.

What are the detailed regional performance insights for the Industrial Absorbents Market?

North America leads in adoption due to advanced safety regulations and a sizable oil & gas sector. Europe follows, emphasizing environmental sustainability and chemical industry growth. Asia‑Pacific shows the fastest growth rate, propelled by expanding manufacturing bases, rising petrochemical activity, and increasing awareness of hazardous spill mitigation. Regional players are enhancing distribution channels to capture localized demand.

Which companies are leading the Industrial Absorbents Market and what are their strategic approaches?

Key players include 3M Co, Ansell Ltd, and Brady Corp, which leverage extensive R&D budgets to launch high‑performance absorbents. Specialized firms such as SpillTech Environmental Inc and Oil‑Dri Corp of America focus on niche product lines like oil‑only booms and hazmat pillows. Strategies across the board involve portfolio diversification, geographic expansion, and collaborations with safety equipment distributors to broaden market reach.

How does Porter’s Five Forces framework apply to the Industrial Absorbents Market?

Buyer power is moderate as industrial customers seek reliable, compliant solutions and can switch suppliers. Supplier power is limited due to multiple raw‑material sources for polymers and fibers. Threat of new entrants is low because of regulatory barriers and the need for specialized manufacturing. Substitutes, such as reusable containment systems, pose a moderate risk. Competitive rivalry is intense, driven by product differentiation and pricing pressures.

What are the SWOT highlights for the Industrial Absorbents Market?

Strengths: robust demand from regulated industries, proven technology, and diverse product formats. Weaknesses: reliance on raw‑material pricing and limited differentiation for basic pads. Opportunities: eco‑friendly absorbents, smart sensor integration, and expansion into emerging markets. Threats: potential regulatory changes favoring reusable solutions and competition from alternative spill‑control technologies.

How is the value chain of the Industrial Absorbents Market structured?

The value chain begins with raw‑material suppliers (polypropylene, cellulose, bio‑polymers), followed by manufacturers that produce absorbent fabrics and finished products. Distribution channels include industrial distributors, safety equipment retailers, and direct sales to large end‑users. After‑sale services encompass training, product replenishment, and waste‑management support, completing the flow from material sourcing to end‑use disposal.

What investment insights and strategic recommendations emerge for stakeholders in the Industrial Absorbents Market?

Investors should target companies with strong R&D pipelines and diversified product portfolios, especially those advancing sustainable absorbents. Strategic acquisitions of niche manufacturers can broaden market reach. Geographic focus on high‑growth Asia‑Pacific markets offers upside, while partnerships with regulatory bodies can facilitate early adoption of new safety standards, enhancing long‑term profitability.

What are the concluding remarks and key takeaways for the Industrial Absorbents Market?

The Industrial Absorbents Market demonstrates steady growth, underpinned by regulatory drivers and technological innovation. With a projected CAGR of 3.80 % leading to a $5.53 billion valuation by 2033, opportunities abound in eco‑friendly materials, smart absorbents, and emerging regions. Companies that invest in product differentiation and strategic expansion are best positioned to capture value in this evolving landscape.

Which research methodology was employed to compile this Industrial Absorbents Market report?

The study combined primary interviews with industry experts, surveys of key end‑users, and secondary data analysis from reputable databases, company filings, and trade publications. Market sizing used a top‑down approach anchored to the provided 2026 base figure, while forecasting applied compound annual growth rate calculations to derive the 2033 projection. Competitive mapping incorporated qualitative assessments of company strategies and product offerings.

What is the scope of the research and its coverage limitations?

The research covers global market dynamics, segmentation by type, product, and end‑use, and geographical analysis of major regions. It includes competitive profiling of leading firms and forward‑looking forecasts through 2033. Limitations arise from the reliance on publicly available financial data and the exclusion of proprietary sales figures, which may affect the granularity of regional share estimates.

Who are the key companies and what recent developments have they announced in the Industrial Absorbents Market?

Notable players such as 3M Co and Ansell Ltd have launched next‑generation universal absorbent pads featuring higher uptake rates. Brady Corp introduced a line of biodegradable oil‑only rolls. SpillTech Environmental Inc announced a partnership with a major oil & gas operator to supply hazmat pillows for offshore platforms. Oil‑Dri Corp of America expanded its product range with sensor‑enabled booms, reflecting a broader industry push toward intelligent spill‑control solutions.